Allworth Chief Investment Officer Andy Stout analyzes what is perhaps the most significant uncertainty affecting the markets.

Last week, as I flew for business over the picturesque Rocky Mountains, there was quite a bit of turbulence. Yet while the bumpy ride was far from pleasant, not once did I wish I had a parachute to use to bale out of the plane.

Understanding that turbulence is sometimes a part of the ride, I know that if I can only focus on where I’m going that I’ll almost certainly get there.

And with that segue, you may well have some understanding about where this is going.

That’s because after all my many years in the financial advice industry, one thing never really changes: some investors want to jump out of the market whenever there is turbulence. But, just as jumping out of a perfectly good plane is a bad idea, we at Allworth Financial believe that jumping out of the market when the atmosphere gets a little bumpy is not a good plan.

Whenever the going gets a little rough, just remind yourself that markets have eventually recovered from every setback in history.

The volatility we’ve experienced to start the year is typical for long-term investors. In fact, just about every two years, stocks experience a drop of at least 10%. And even though the catalyst for volatility changes, it’s often rooted in uncertainty.

Inflation

One of the most significant uncertainties in today’s environment is the potential fallout from inflation. It’s not just the path that inflation may take over the next several months that’s uncertain, but it’s also the reaction to inflation by our nation’s central bank, the Federal Reserve (Fed). That is, how the Fed responds to inflation will affect the economy and the stock and bond markets.

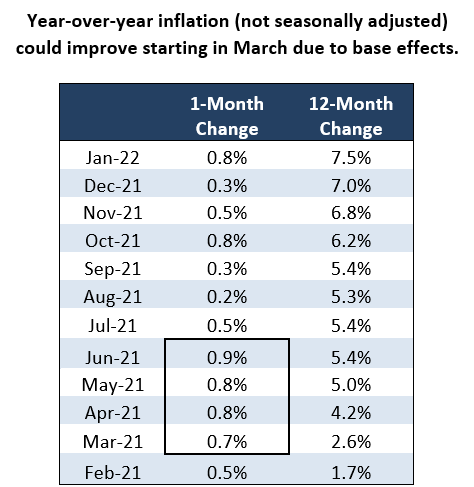

Last month, we stated, “We expect inflation to continue to get worse for a few more months before easing later this year.” That’s precisely what’s happened so far, and unfortunately, inflation will likely be even higher when we get the February data.

The latest release of CPI (Consumer Price Index) showed that consumer inflation was 7.5% for the 12 months ending on January 31, making it the highest reading since way back in February of 1982. (Early estimates for February’s year-over-year inflation rate are around 7.8%.)

What could cause inflation to get better later this year?

Fortunately, inflation could begin to subside in a couple of months. While many of the root causes of high inflation will still be a problem, the simple fact is that the exceedingly high monthly inflation changes of March, April, May, and June 2021 will no longer be in the year-over-year numbers as the year progresses. (It’s known as “base effects” when a year-over-year number changes because data from a new month replaces an old month.)

Beyond base effects, there are a couple of other substantial reasons that inflation should improve throughout the year:

- A Shift in Spending

While it’s too early to predict a return to normal spending habits, there are early signs that consumers are beginning to increase their relative spending on services compared to goods. For example, when the economy shut down in March 2020 for a few months, consumers immediately increased their proportional spending on goods.

Specifically, relative goods expenditures rose from 36% to 40% in just two months. This 4% move is not as trivial as it appears because that is 4% on nearly $14 trillion of annual spending, equating to more than half a trillion dollars.

In March 2021, relative spending on goods peaked at 41.6%, and service spending fell to 58.4%. But now, the most recent data shows that goods spending is at 38.8%, and service spending represents 61.2%.

This shift matters because goods spending takes a much larger toll on the supply chain, leading to a more significant supply-demand imbalance. And that imbalance results in higher prices.

- Living with the Virus

Evidence is mounting that people are becoming more comfortable with the virus. We’re seeing this even as new cases skyrocketed to more than 1,000,000 per day in early January. Fortunately, cases have quickly fallen, hovering around 100,000.

Even as virus cases climbed over the past year, credit card transactions that required people to be present (as opposed to online purchases) were higher than what they were before the pandemic.

Another example of people getting out to spend can be found in the latest retail sales report, which showed retail sales (not including online spending) rose 4.4% last month, and they’re 18.3% higher over the past year.

Businesses have also adapted. This can be seen in capacity utilization, which measures the percent that installed capacity is being used. For example, a reading of 100% would mean that a company’s factories are never idle; they’re constantly producing goods.

By analyzing US manufacturing companies as a whole, we observe that factories have fully recovered and are operating at a level similar to a normal economic environment.

What could cause inflation to remain more elevated than pre-pandemic levels?

While there are reasons suggesting inflation will decrease, there are also reasons that inflation will not drop to the Fed's goal of 2% in the near future. Here are some of the factors that will likely keep inflation elevated (yet still lower than where we are currently):

- There are 4.6 million more job openings than unemployed people. This spread suggests that employees have the upper hand in demanding higher wages. Currently, average hourly earnings are 5.7% higher over the past year, but certain industries are seeing more wage pressure than others. For example, hourly wages for leisure and hospitality workers are 15% higher than a year ago.

- Russia/Ukraine tensions could keep oil and gasoline prices high. Should economic sanctions cause Russia’s massive oil supply to be cut off from other parts of the world, the cost of oil could keep energy prices elevated.

- Housing inventory is at a record low. With so few houses for sale, sellers demand higher prices to part with their homes. Because housing costs make up 32.9% of CPI, we expect current inventory levels to keep a floor under inflation.

- Supply chain dislocations – while better – are still present. On the positive side, shipping costs, manufacturing backlogs, and capacity utilization have improved. These are early signs of a recovery. However, on the negative side, the supply chain recovery has a ways to go. Comprised of 27 variables, the Global Supply Chain Pressure Index shows how far from average (as measured by standard deviations) the supply chain is functioning.

The Federal Reserve has begun to fight inflation

The Fed has become increasingly worried about inflation, and its members have been extremely vocal about stopping it. This "Fedspeak" has caused interest rates to rise in anticipation of the Fed aggressively hiking short-term interest rates.

Just six months ago, the market anticipated one rate hike this year. At the beginning of this year, that expectation had risen to three rate hikes. But today, the market is pricing in a little more than six rate hikes in 2022.

As the Fed raises short-term interest rates, it makes loans more expensive. With a higher cost of borrowing, consumers might spend less, which could help bring down inflation.

The risk is that the Fed makes a mistake, causing monetary policy to be too restrictive (i.e., it hikes rates too quickly for the economy to handle in stride). Because longer-term interest rates often track expected economic growth, we could see those interest rates drop (and bond prices rise).

What does this mean for you?

At the beginning of this article, I mentioned that uncertainty is often the cause of volatility. There are, of course, other sources of uncertainty besides inflation. Current examples are tensions between Russia and Ukraine, whatever the next Covid strain is, and China’s economy.

It’s not only necessary to understand the sources of uncertainty, but one must also think a few steps ahead to grasp the relationship between the sources mentioned and their potential ripple effects. For example, many connections lie between a tight labor market and the present value of a stock’s future earnings.

Understanding that and many other complex relationships allows us to help set your investment mix to support your financial plan and retirement.

February 18, 2022

All data unless otherwise noted is from Bloomberg. Past performance does not guarantee future results. Any stock market transaction can result in either profit or loss. Additionally, the commentary should also be viewed in the context of the broad market and general economic conditions prevailing during the periods covered by the provided information. Market and economic conditions could change in the future, producing materially different returns. Investment strategies may be subject to various types of risk of loss including, but not limited to, market risk, credit risk, interest rate risk, inflation risk, currency risk and political risk.

This commentary has been prepared solely for informational purposes, and is not an offer to buy or sell, or a solicitation of an offer to buy or sell, any security or instrument or to participate in any particular trading strategy or an offer of investment advisory services. Investment advisory and management services are offered only pursuant to a written Investment Advisory Agreement, which investors are urged to read and consider carefully in determining whether such agreement is suitable for their individual needs and circumstances.

Allworth Financial and its affiliates and its employees may have positions in and may affect transactions in securities and instruments mentioned in these profiles and reports. Some of the investments discussed or recommended may be unsuitable for certain investors depending on their specific investment objectives and financial position.

Allworth Financial is an SEC-registered investment advisor that provides advisory services for discretionary individually managed accounts. To request a copy of Allworth Financial’s current Form ADV Part 2, please call our Compliance department at 916-482-2196 or via email at compliance@allworthfinancial.com.

January 12, 2024

Fourth Quarter 2023 Market Update

January 12, 2024

Fourth Quarter 2023 Market Update

Allworth's Co-CEO Scott Hanson and Chief Investment Officer Andy Stout team up for this fourth quarter 2023 market update video.

Read Now December 15, 2023

December 2023 Market Update

December 15, 2023

December 2023 Market Update

Chief Investment Officer Andy Stout takes a look back on the year to help give perspective to what's on the horizon in 2024. At the beginning of this …

Read Now November 17, 2023

November 2023 Market Update

November 17, 2023

November 2023 Market Update

Chief Investment Officer Andy Stout examines whether there’s a chance the US dollar will lose its status as the world’s reserve currency. There is a …

Read Now